When the world gets loud, the group chat gets louder

Explore how geopolitical volatility impacts markets and trading decisions. Understand the gap between market data and actionable plans.

By Priyanka Joshi · Vice President of Content & Marketing at Deriv

18 March 2026 · 5 min read

My WhatsApp group hasn't stopped buzzing since geo-political tensions escalated trading insights with US–Israel war on Iran.

From that distant US cousin to a mate from university I haven't spoken to since 2019. My mum's friend's son who "does a bit of crypto.” They all want to know if I’m trading oil/gold/silver/gas/WTI futures/Crypto/forex ?

I can't tell them. Not because I don't have views — I do, plenty — but because giving trading advice to folks like these who check their portfolio once a quarter is like handing car keys to someone who's never seen a roundabout. Your risk appetite, your time horizon, your ability to sit still when the screen turns red — I don't know any of that about you. And frankly, you probably don't either.

So here's what I'll offer instead. Observation.

Things I've picked up sitting near traders this week, and from watching markets run this exact playbook before.

How markets actually behave during geopolitical shocks — and why most people get it wrong

Stock markets almost always overreact to the initial shock of a geopolitical event and recover within six months. Carson Group analysed 40 major geopolitical events across 85 years (from Pearl Harbor to the Russian invasion of Ukraine) and found the S&P 500 dropped an average of 0.9% in the first month, then gained 3.4% by month six. The pattern holds across wars, assassinations, oil embargoes, and territorial invasions. The critical variable isn't the severity of the event — it's how long the uncertainty persists before markets reprice it as the new normal.

The 2026 Iran conflict is following this pattern precisely.

On 3 March, the Dow closed down about 400 points, while Brent popped into the low-$80s. A few days later, oil decided it wanted to cosplay 2022 again! On 9 March, Brent briefly ripped to around $119.50 intraday, then by 10 March it was back down near the low-$90s after the headlines shifted. Outside the US, the damage looked uglier: Pakistan’s KSE-100 dropped 9.57% on 2 March, and South Korea’s KOSPI fell about 12% on 4 March, triggering circuit breakers for the first time since August 2024. India’s VIX flared roughly 50–60% over two sessions. In the US, the VIX hit an intraday high around 28.15 on 3 March, the highest level of 2026 so far.

Every one of those numbers is consistent with the historical pattern. Every one of them looks terrifying in isolation and ordinary in context.

The geopolitical volatility gap: why information isn't a trading plan

There's a concept I keep coming back to in weeks like this, and I've started calling it the geopolitical volatility gap. It's the distance between knowing what markets typically do during a crisis and knowing what you should do with your portfolio during one.

Most people confuse the two. They read that markets recover, which is historically true, and treat it as a buy signal. Or they see a 12% oil spike and panic-sell everything. Both responses mistake information for a plan. The information is the same for everyone. The plan depends entirely on your time horizon, your risk tolerance, your liquidity needs, and frankly your ability to not touch anything for six months while the headlines stay ugly.

That gap is where retail money gets destroyed during geopolitical volatility. Not from a lack of data. From mistaking data for a decision.

Two wars that explain this one

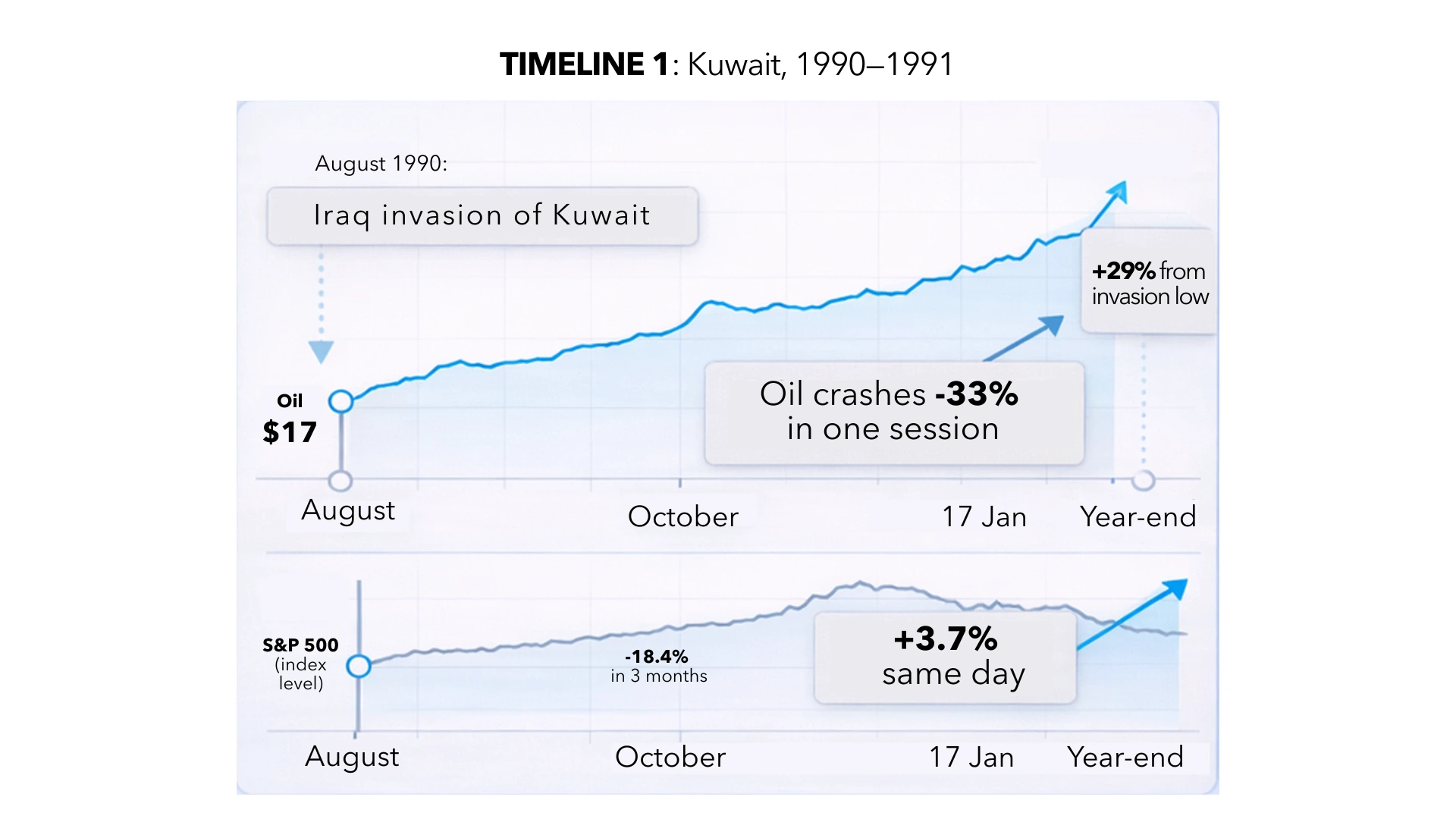

Kuwait, 1990. Iraq invades in August. Oil doubles — from $17 to $36 a barrel by October. The S&P 500 drops 18.4% in three months. Every financial commentator on the planet is calling a prolonged bear market.

Then, on January 17, 1991, Operation Desert Storm launches. Oil crashes 33% in a single session. The S&P gains 3.7% the same day. Within four weeks, it's up 17.6%. By year-end, the index has climbed 29% from the invasion low.

The people who sold in October 1990 locked in the worst possible price and watched the recovery from the sidelines.

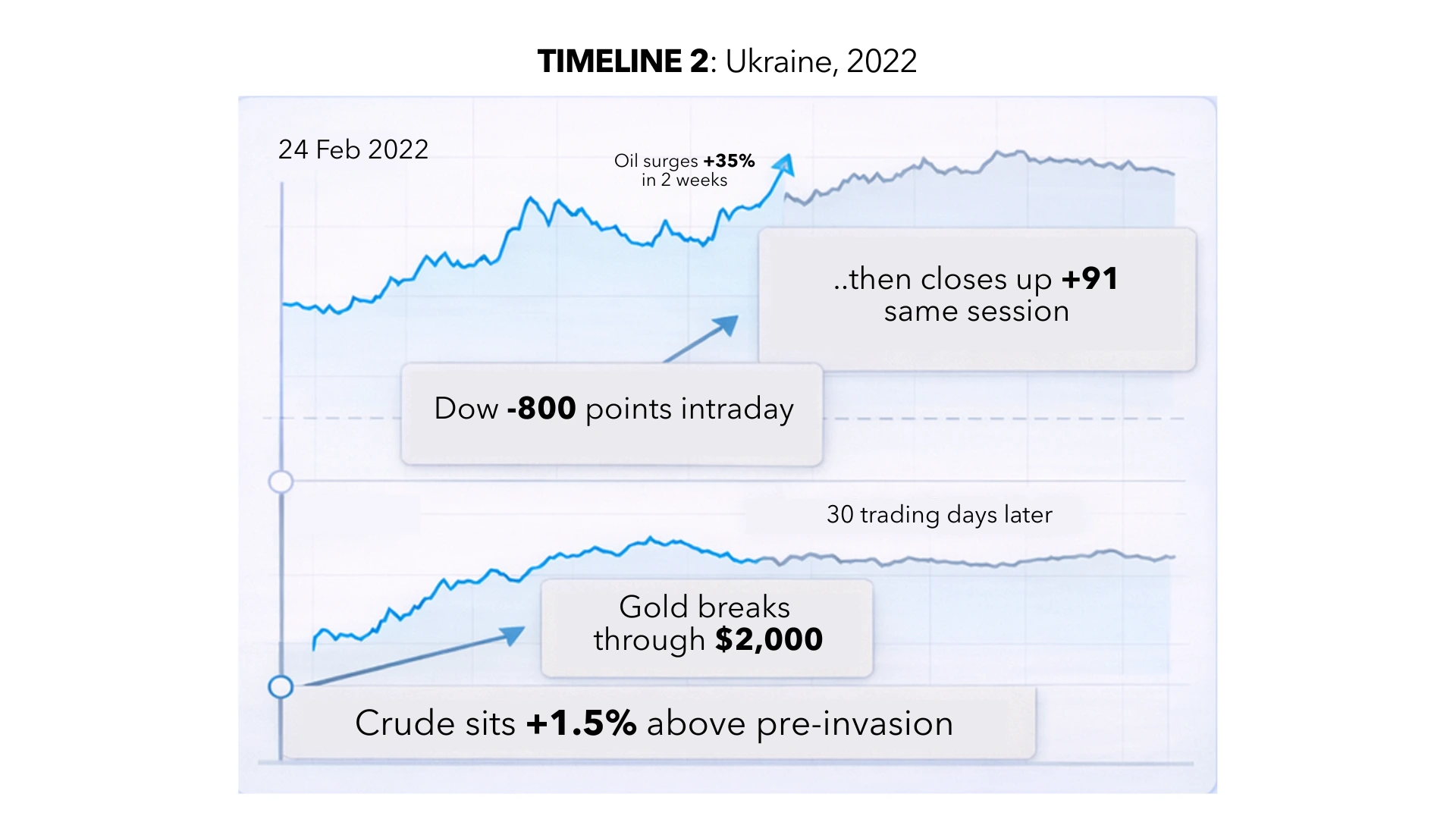

Ukraine, 2022. Russia invades on February 24th. Oil surges 35% in two weeks, punching past $100 for the first time since 2014. The Dow swings 800 points down intraday, then closes up 91. Same session. Gold breaks through $2,000. The consensus view is that globalisation is finished. Thirty trading days later, crude is barely 1.5% above pre-invasion levels.

Neither war was identical. Neither had the same actors, stakes, or geography. But the market mechanics rhymed: a violent spike in fear-driven assets, a flight from risk, and then a recalibration once the initial shock stopped being new information and started being priced-in reality.

The pattern doesn't guarantee the outcome. But it does suggest that the first week's price action is almost never the final answer.

What the traders around me are actually saying expert trading strategies

I sit near people who do this for a living. Not pundits. Not influencers. People with live risk on the screen. Here's what I keep hearing:

"Everyone's an oil expert this week." One of them said this on Monday, scrolling through LinkedIn. He's been trading energy for fourteen years. His actual position? Smaller than you'd expect. Because the real risk, he says, isn't direction but duration! If the Strait of Hormuz stays navigable (it handles roughly 21 million barrels a day — about a fifth of global oil consumption, with 84% bound for Asian markets including China, India, Japan, and South Korea), this is a two-week trade. If shipping gets choked, it's a structurally different market. Nobody can model that binary with confidence.

"Gold does what gold always does." Spikes on fear. Fades once the fear becomes furniture. It's a brilliant short-term hedge and a mediocre position if you're buying at the top of a panic. Every time, without fail, retail money piles in at the fear spike and then sits through months of sideways drift wondering what went wrong. Gold's value during geopolitical shocks is as a hedge you already own, not one you buy after the headlines break.

"The interesting trade is in what nobody's watching." While the world stares at crude tickers, European natural gas has nearly doubled on the back of attacks on Qatari LNG facilities. Defence stocks are moving. Shipping and freight rates are repricing. Insurance premiums for Gulf transit are climbing. The Strait of Hormuz story isn't just an oil story — it's a logistics story, an inflation story, and a central bank story all at once. If elevated energy prices persist, the eurozone faces a potential 0.5% inflation bump and the Fed's rate-cut calculus shifts entirely. Treasury yields are already climbing as traders price in the possibility that cuts get pushed back. That's the second-order move most people are missing while they argue about the price of a barrel.

The VIX at 27 tells you the market is nervous and not that the market is right.

Why duration matters more than direction

The debate on every trading floor, every group chat, every Twitter/X Space hot take is about direction: will oil go up or down, should I buy or sell, is this bullish or bearish.

The actual question — the one serious traders are asking — is about duration. How long does the disruption last? A contained, short-duration conflict with no sustained Hormuz closure is a volatility event. Markets spike, then normalise. That's Kuwait. That's Ukraine. That's the base case most institutional desks are currently working with.

A prolonged disruption to Gulf shipping, on the other hand, is a supply shock. Supply shocks feed into inflation. Inflation feeds into central bank policy. Central bank policy feeds into credit conditions, corporate earnings, and the entire risk-asset pricing framework. That's a different trade entirely — not a two-week VIX spike but a structural repricing that could take quarters to work through.

The duration question is binary and unmodelable. Which is exactly why the smartest traders I know are running smaller positions than you'd expect, not larger ones.

So what do I tell my cousin?

Here's what I tell him when he asks again and he will ask again:

Markets have absorbed wars, assassinations, oil shocks, and invasions for nearly a century. The initial move is almost always sharper than the follow-through. Panic selling has a near-perfect track record of being the wrong decision six months later.

But that's a statistical observation about indices. It is not a recommendation for his portfolio. Or yours. The distance between "historically, markets recover" and "you should buy the dip on Tuesday" is enormous. It's the distance between reading a weather forecast and sailing across the Atlantic. One is information. The other requires knowing your boat, your crew, and how much seasickness you can stomach. Geopolitical volatility gap is mistaking “news/information” for a plan.

Also the reason why I still can't answer the text.