Japan intervention impact on yen carry trade

Japan intervention impact grows as yen carry trade pressure drives sharp USDJPY movements

By Prakash Bhudia · Global Trading Strategist & Technical Markets Expert

30 April 2026 · 6 min read

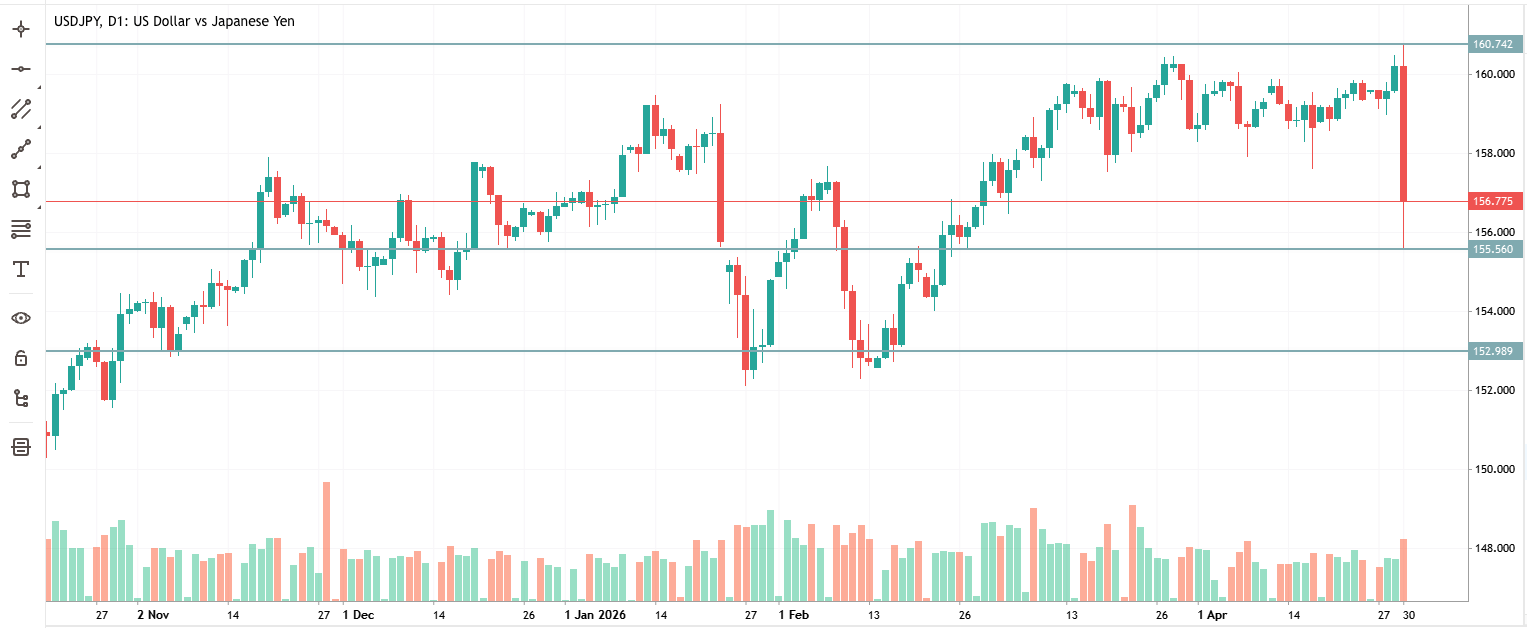

USD/JPY intraday range today — 160.73 high to 155.55 low — triggered by Japanese intervention warnings

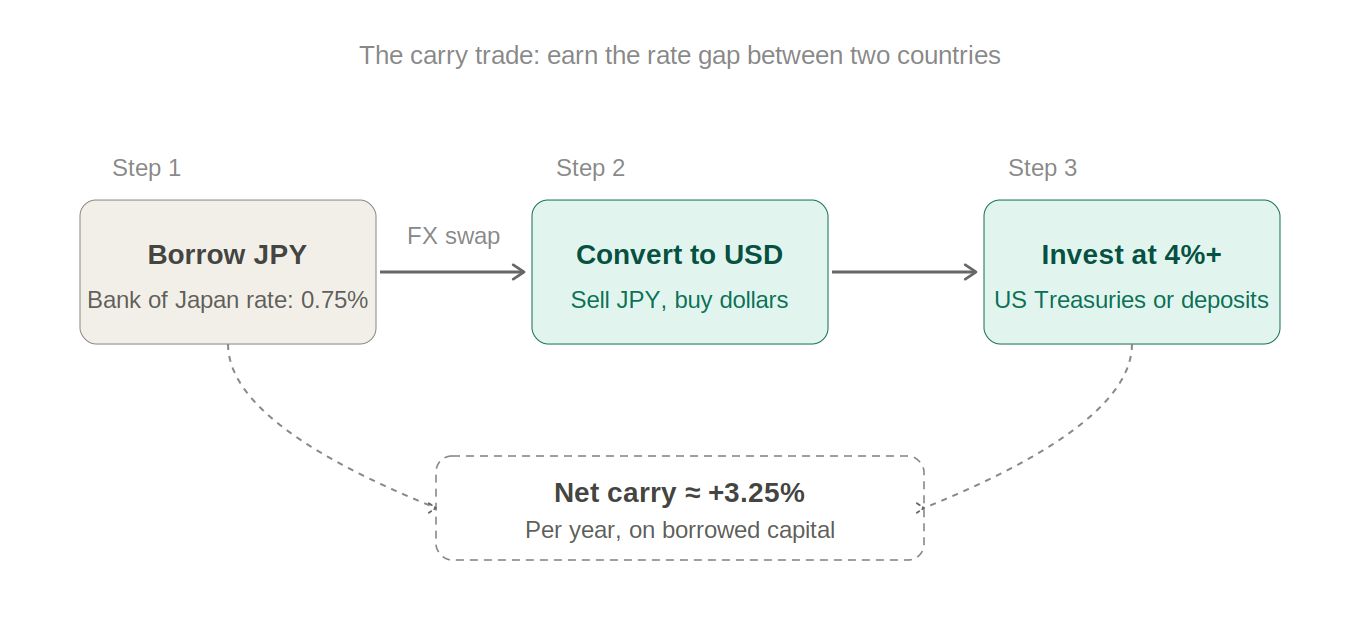

The trade everyone piled into

For years, one trade dominated FX markets forex trading strategies FX trading strategies: borrow money in Japan at near-zero interest rates, convert it to dollars or Australian dollars, park it somewhere that pays 4–5%, and pocket the difference. It’s called the carry trade, and at its peak it was the most crowded position in global finance.

The logic is simple. Japan’s central bank kept rates pinned to the floor for decades. While every other major central bank was raising rates aggressively after 2022, Japan barely moved. That gap — the differential between what you pay to borrow in yen and what you earn investing elsewhere — was free money, as long as the yen didn’t strengthen.

So everyone did it. Hedge funds, pension managers, retail traders. When a trade works for that long, it stops being a trade and becomes a consensus. And when a trade becomes a consensus, the positioning data tells you exactly how dangerous it is: as of this week, speculative short-yen positions are the largest they’ve been since July 2024.

Why Tokyo can’t just watch

Japan imports almost everything it needs to run its economy — oil, gas, food commodities, industrial materials. When the yen weakens, every one of those imports gets more expensive in yen terms. That’s imported inflation, and it hits ordinary Japanese households directly at the petrol station and the supermarket.

With Brent crude above $120 a barrel today — driven by Middle East tensions — the pressure is acute. A weak yen on top of an oil shock is a political problem, not just an economic one. Finance Minister Satsuki Katayama can only issue so many verbal warnings before inaction starts to look like incompetence.

The 160 level has become a psychological line. It’s not a law of physics — but markets know that Japan has acted near this level before, which means everyone watches it, which means it becomes self-fulfilling. Cross 160, and the intervention clock starts ticking louder.

How Japan actually intervenes

The mechanics are straightforward. Japan’s Ministry of Finance authorises the action. The Bank of Japan executes it — selling US dollars from Japan’s foreign exchange reserves and buying yen. More yen demand means a stronger yen. Simple in theory, brutal in practice when the scale is large enough.

Japan has done this before at scale. In 1998, during the Asian financial crisis, coordinated intervention with the US stopped a yen freefall. In 2011, after the Tohoku earthquake sent the yen surging too strong, Japan intervened to weaken it. In 2022, the yen was collapsing through 145, then 150 — Japan spent roughly $60 billion in reserves to defend it. It worked, temporarily.

Today’s move looks like a combination: the Finance Minister’s “decisive action” language was the strongest signal yet, and market sources noted the price action bore the hallmarks of actual official buying — though no confirmation has come. The distinction matters because words fade; reserves don’t.

The short squeeze: When crowded trades get hit

Here’s why 520 pips happened so fast. When everyone is on the same side of a trade — in this case, short yen — and something forces a reversal, the exit door is tiny. Every short position that starts losing money has a stop-loss level where it automatically closes. Those closures generate more buying pressure, which triggers more stops, which forces more liquidations.

It’s like a theatre fire where everyone rushes the same exit. The move isn’t proportional to the actual policy change, it’s proportional to how many people were positioned wrong. The more crowded the trade, the more violent the squeeze.

This is one of the most important concepts in trading: the size of a move is not just about the news. It’s about how many people were on the wrong side when the news hit.

Stops were likely clustered just below 158 and again at 155 — exactly the levels that turned a sharp move into a cascade. Each cluster that triggered added fuel to the next leg down.

Can Japan actually win this fight?

Japan holds roughly $1.1 trillion in foreign exchange reserves, mostly US Treasuries. That sounds enormous and it is. But intervention burns through reserves fast when you’re fighting a structural trend. The 2022 effort cost around $60 billion and bought a few months of breathing room before the yen resumed weakening.

There’s a brutal feedback loop at work. When Japan sells US Treasuries to fund yen purchases, it pushes US Treasury yields higher. Higher US yields make the dollar more attractive. That widens the interest rate differential between the US and Japan which is the very reason the carry trade exists in the first place. Japan is pouring water into one end of the bath while the other end drains.

The only structural fix is a BOJ rate hike, raising the cost of borrowing yen makes the carry trade less profitable and reduces the fundamental pressure on the currency. The BOJ held at 0.75% this week. Markets are pricing a June hike as the most likely next move, but “most likely” in this environment means maybe 40%.

What’s actually happening here — and what to watch

This is a positioning unwind, not a structural shift — unless the BOJ moves. The fundamentals that built the carry trade haven’t changed overnight — the rate differential is still wide, oil is still expensive, and the BOJ hasn’t moved. What changed today is that a crowded short got squeezed by a credible threat. Those moves are sharp but they don’t always stick.

Momentum traders are riding the squeeze for as long as shorts keep covering. Retracement buyers are waiting for the yen to give back ground once the panic clears. Options traders are simply pricing volatility — when governments step into markets, uncertainty itself becomes the trade.

TRADER TAKEAWAY

Watch 155. If it holds, expect a grind back toward 158 as the squeeze exhausts itself. If it breaks, the unwind has further to run — next support sits around 152–153. A confirmed BOJ rate hike in June would be the first signal that the structural yen weakness is actually turning. Until then, interventions buy time, not trend change.