Hormuz: The world’s economic pinch point

Manaf Zaitoun

March 19, 2026

6

min read

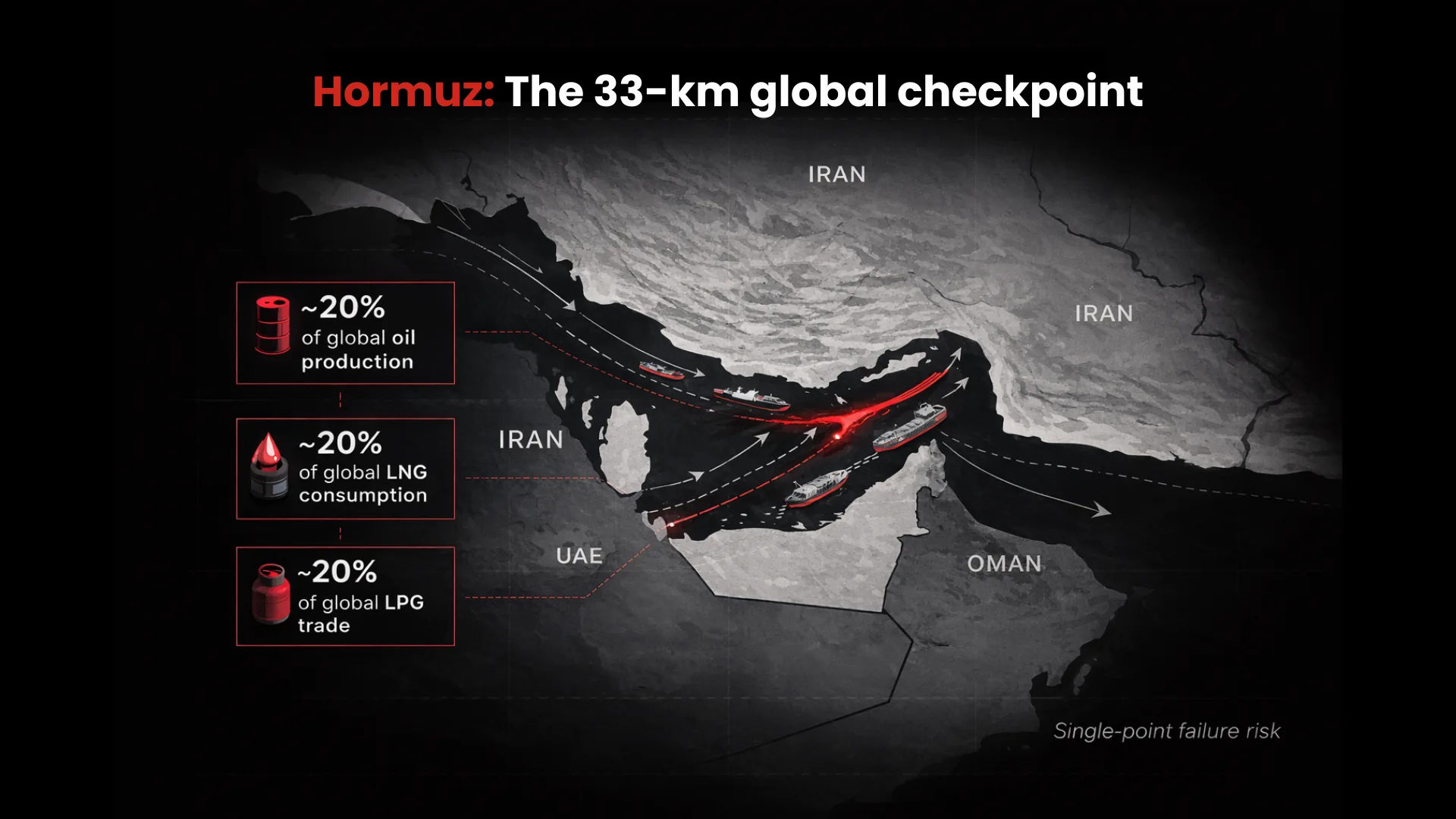

When a new war breaks out, we often focus on the “big moves,” such as shifting borders or the rise of superpowers. But in March 2026, the most significant threat to your bank account, your dinner table, and even the phone in your pocket isn’t a border dispute; it’s a 33-km-wide strip of water.

The Strait of Hormuz is often lazily categorised as an “energy chokepoint.” While it is true that it sits at the heart of the world’s hydrocarbon trade, viewing it solely through the lens of oil and gas is a dangerous oversimplification. It’s the primary passage through which millions of tons of materials that make modern life possible pass every day. When it’s blocked, the disruption doesn't just slow the energy markets; it risks global economic paralysis.

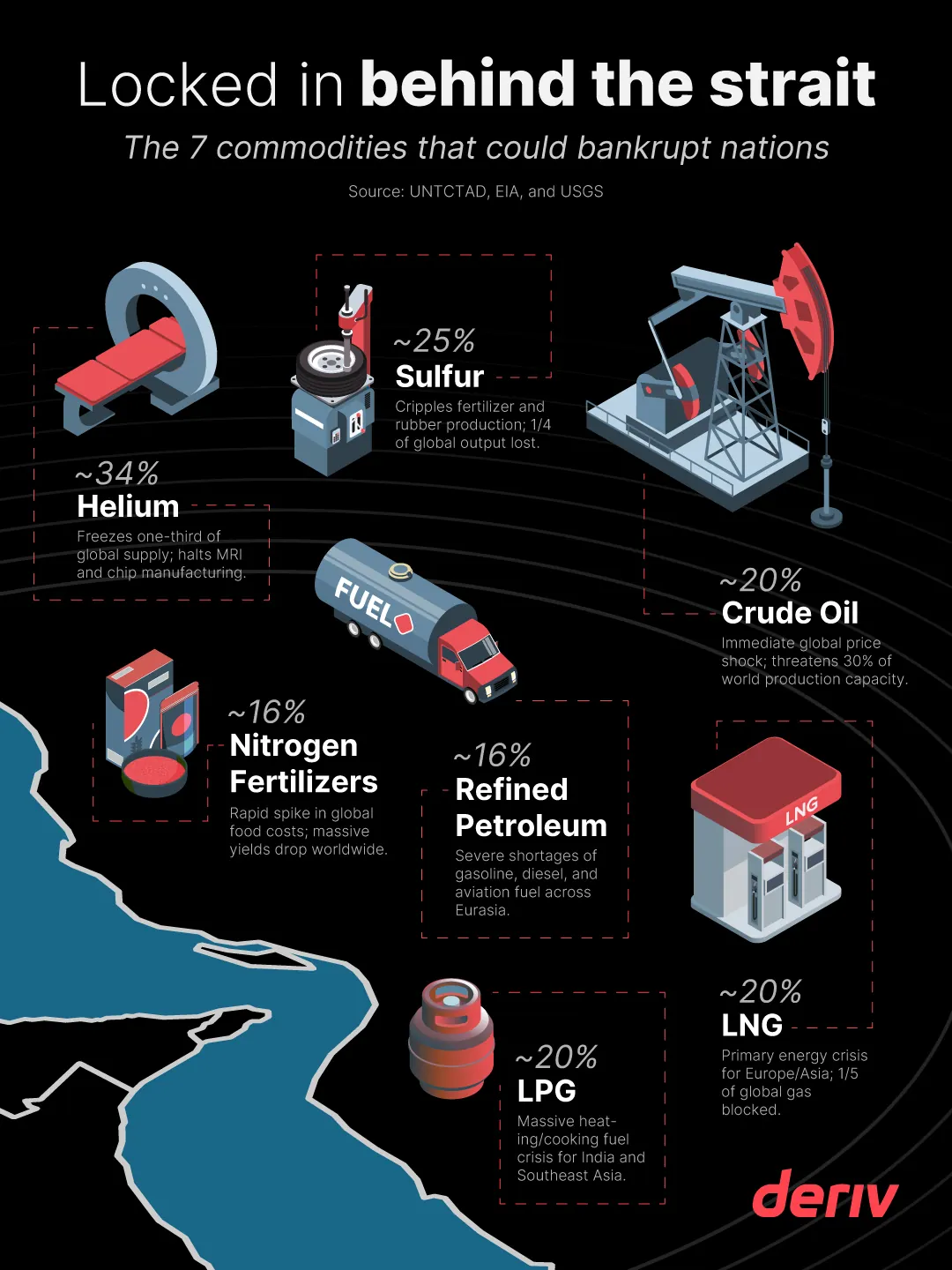

To understand the danger of disruption, one must look beyond the tankers and into the cargo hold. The commodities flowing through the Gulf are the building blocks of several major industries, from agriculture to high-tech manufacturing.

The most critical flow is Crude Oil, the lifeblood of global transportation and industry. As per U.S. Energy Information Administration (EIA) 2026 figures, roughly one-fifth (about 20%) of the world’s total oil production is produced behind this chokepoint. This oil is essential not only for running cars and generating electricity but also for other raw materials, affecting industries from logistics and automotive to general manufacturing.

However, the risk extends far beyond crude oil. As reported by the U.S. Geological Survey (USGS), Helium presents a more "invisible" danger; as a non-synthesizable byproduct of natural gas extraction, Qatar's position as the world's second-largest producer means a blockade effectively deletes one-third (about 34%) of the global supply. This would severely impact the medical sector (MRI cooling), semiconductor manufacturing, and the aerospace industry. Additionally, according to 2026 industry data from Argus Media, the Gulf accounts for roughly a quarter (about 25%) of the world's Sulfur output, a byproduct of oil and gas desulfurisation. Without it, the world cannot produce sulfuric acid, a "workhorse" of the chemical industry, which is vital for phosphate fertiliser production, rubber vulcanisation (tyres), and paper manufacturing.

The global energy transition has actually heightened reliance on the region for natural gas. According to UNCTAD’s March 2026 Rapid Analysis, one-fifth (about 20%) of the world's Liquefied Natural Gas (LNG) consumption passes through the Strait, primarily destined for Europe and East Asia, impacting electricity generation, heavy heating, and industrial chemicals. Furthermore, figures from the International Fertilizer Association (IFA) show that Urea/Nitrogen Fertiliser production in the region accounts for 16% of the total world output. Natural gas is the primary feedstock for urea, meaning if the gas stops flowing, the fertiliser stops being made, which directly threatens global agriculture and food processing.

Finally, the Gulf's role has expanded beyond "raw" crude. Per International Energy Agency (IEA) and OSW infrastructure reports, massive mega-refineries now process diesel, gasoline, and jet fuel locally, contributing about 16% of the world's refined petroleum products—a supply critical for commercial aviation, shipping, and last-mile delivery. Similarly, UNCTAD 2026 trade data indicates that about 20% of the world's Liquefied Petroleum Gas (LPG), a primary cooking and heating fuel for hundreds of millions in developing economies (particularly in Southeast Asia and India), passes through this vital chokepoint, also affecting the petrochemical industry.

.webp)

In short, very few products won’t be affected by a shipping blockade at the Strait, and an overall economic crisis is as likely as the much-anticipated energy crisis.

.webp)

The timing of the current 2026 instability in the Gulf could not be worse. The global economy is still suffering from the scars of two major macrocrises that fundamentally disrupted the traditional supply chain model.

First, the COVID-19 pandemic taught us that "just-in-time" manufacturing was a house of cards. It created a massive backlog in logistics that took years to clear. Second, the Russia-Ukraine war triggered a structural shift in inflation, particularly in energy and food. Before these events, the world had a "buffer." Today, there is no buffer.

Central banks have spent the last few years fighting the stickiest inflation in forty years. A disruption in the Middle East now doesn’t just raise prices; it triggers a new wave of inflation. Unlike the previous waves, which were driven by demand spikes or regional land-war sanctions, a Hormuz blockade is a supply-side amputation. You cannot "interest rate" your way out of a 34% drop in Helium or a 16% drop in global fertilisers. If the goods physically cannot move through the water, the price becomes irrelevant because the supply simply does not exist.

On the other hand, the current marker drivers are at risk as well. Two industries are going to be sensitive to these disruptions, and that’s the ones we associate with the “future”: Artificial Intelligence (AI) and Crypto.

The AI boom is powered by massive data centres that have two insatiable needs: electricity and advanced chips.

AI training is incredibly energy-intensive. As LNG and Oil prices spike, the cost of running “compute” becomes astronomical, potentially bankrupting smaller AI startups and slowing the pace of innovation for tech giants. The Helium shortage mentioned earlier is a direct threat to the semiconductor industry. Without high-purity helium, the ultra-cold environments required for certain stages of chip lithography are impossible to maintain. A blockade in the Gulf could lead to a multi-year "chip winter." We already had a peek at how fast a semiconductor shortage can paralyse industries between 2020 and 2023.

On the other hand, the crypto market has always been a high-beta play on global liquidity and energy. When energy costs rise, the "hash rate" profit margins collapse. We could see a massive consolidation of miners, leading to increased centralisation of the networks.

Also, crypto remains a "risk-on" asset. In the event of a prolonged blockade, capital will flee to "safe havens" such as gold or short-term treasuries, potentially triggering a massive liquidity drain in crypto markets that mirrors the 2022 crashes. If coupled with hawkish Fed policy, a crypto winter is almost certain.

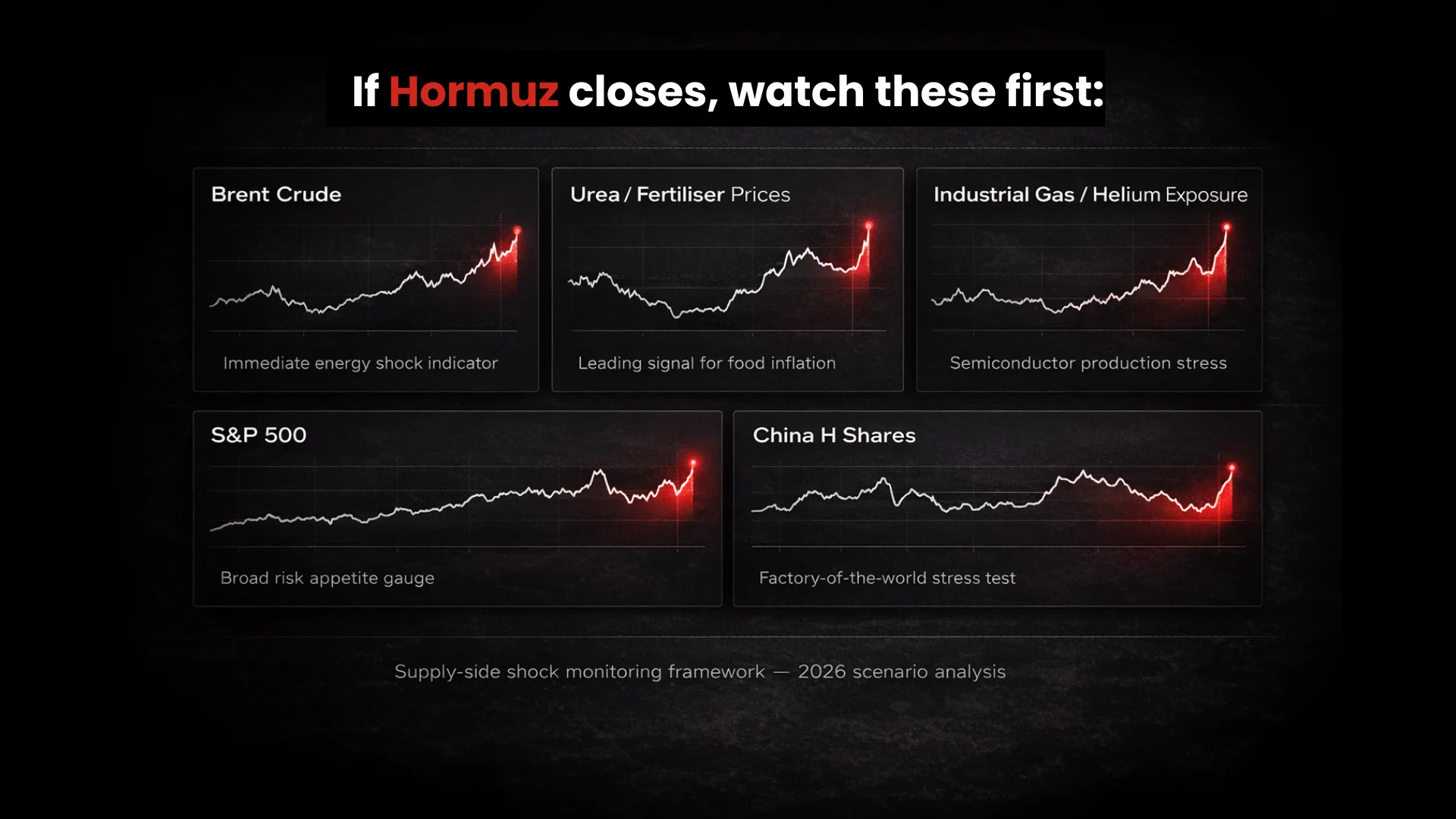

If you are a trader or an investor in 2026, watching "Brent Crude" is no longer enough. To survive a Gulf disruption, you must widen your lens.

Watch the price of Urea and Potash. If the Gulf closes, these will spike before food prices do. Tracking the fertiliser sector provides a leading indicator for the next wave of grocery store inflation.

Since Helium isn’t traded on a standard commodity exchange like oil, track price movements in the industrial gas sector by following ETFs like UNG.US. The ability of major gas suppliers to fulfil contracts will tell you more about the health of the tech sector than the NASDAQ-100 will.

The S&P 500 and the Euro Stoxx 50 are vulnerable, but China is the wildcard. China is the largest importer of Gulf energy and the largest exporter of manufactured goods. If China’s energy costs double overnight, its "factory of the world" status falters, leading to a massive drag on the China H Shares index and global retail prices.

The Strait of Hormuz is not just a geographical location; it is a global economic nervous system. This 33-km-wide passage might affect whether we can feed our populations, power our AI, and maintain our digital economies. For the savvy observer, the goal is to look past the headlines of war and see the invisible lines of unsung commodities that truly keep the world turning.

Disclaimer: This content is not intended for EU residents.

Comments (-)