Geopolitical impact of Hormuz architecture

Explore how the Hormuz architecture affects global markets and energy dynamics, with key insights for investors on geopolitical implications.

By Sahil Shah · Trading Operations & Risk Strategy Expert

1 April 2026 · 2 min read

The end of the "Shadow War"

For years, the friction between the United States, Israel, and Iran was confined to the shadows—cyberattacks, proxy skirmishes, and maritime harassment. That era ended on February 28, 2026. The joint U.S.-Israeli air campaign against Iranian nuclear and command infrastructure has fundamentally reordered global markets energy market insights, turning "geopolitical risk" from a secondary variable into the only variable that matters.

As we close out March, the data reveals a market in a state of high-velocity transformation. The traditional relationship between energy and safe-haven assets has fractured, creating a "divergence" that is catching even seasoned institutional investors trading strategies off guard.

The weaponisation of the Strait

In the thirty days since the first strikes, Crude Oil has undergone its most aggressive monthly rally in modern history. While the initial military action caused a calculated 13% jump, the true "gamma flip" occurred when the Iranian Revolutionary Guard successfully executed a total blockade of the Strait of Hormuz.

The arithmetic of this blockade is devastating. With approximately 20% of global oil and 25% of Liquified Natural Gas (LNG) currently stranded, the world is facing a structural deficit of nearly 12 million barrels per day.

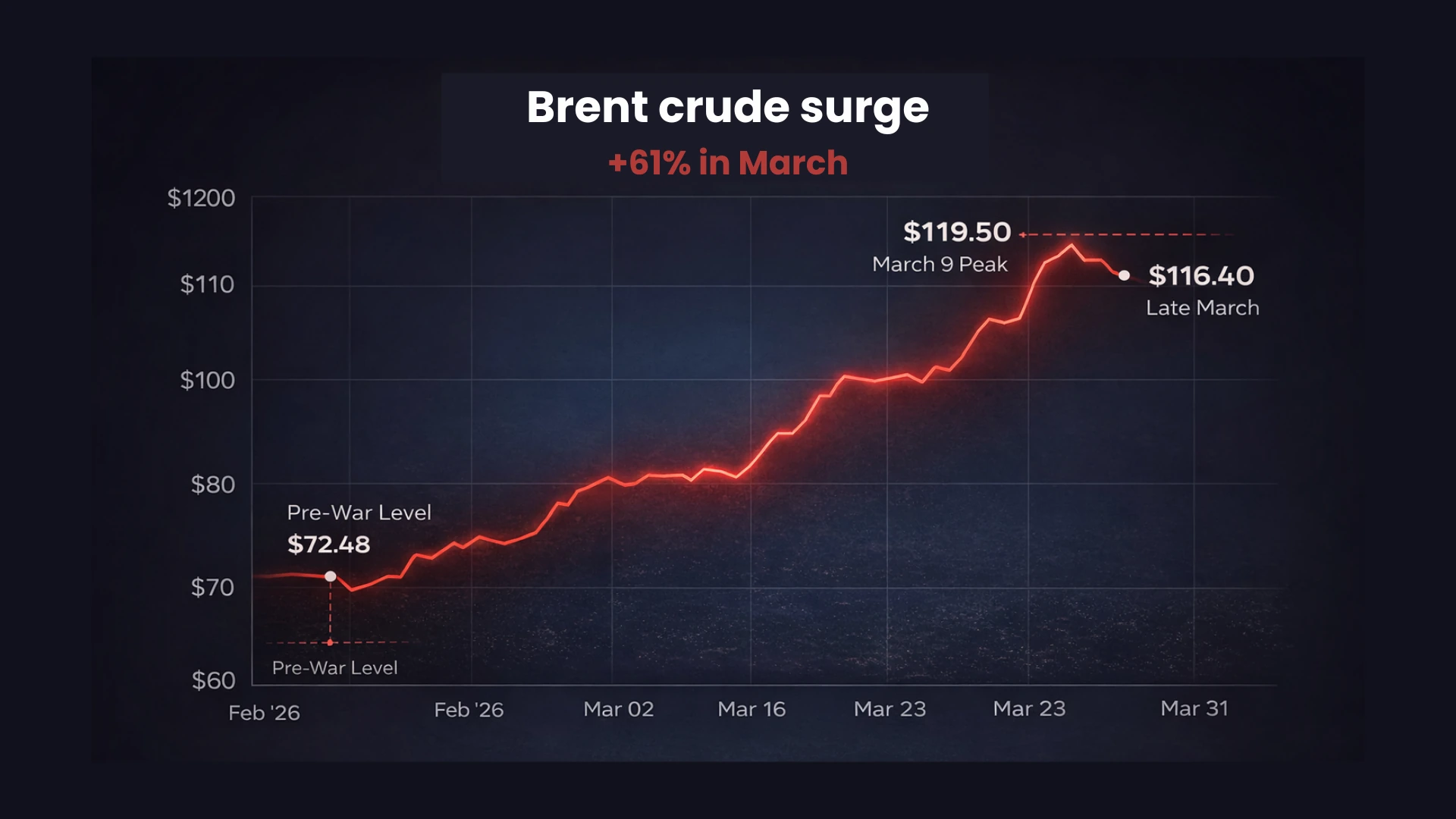

Brent Crude, which sat comfortably at $72.48 on the eve of the war, peaked at an intraday high of $119.50 on March 9. Even after a record-breaking release of 400 million barrels from the International Energy Agency (IEA) reserves, the market remains fixated on the physical reality: a strategic reserve release is a temporary band-aid for a severed artery. Today, Brent hovers near $116.40, a staggering 61% increase in a single month. This isn't just a price hike; it is a "tax" on global productivity that is currently pushing European and Asian GDP forecasts toward a recessionary floor.

The gold paradox

Perhaps the most shocking data point of March 2026 is the behavior of gold. In a textbook conflict, gold and oil move in tandem as investors flee "paper" assets for hard commodities. Instead, we are witnessing a historic decoupling.

Gold initially surged to $5,246 as the strikes began, but as the war intensified, the price collapsed. By mid-March, gold began a steep descent, losing nearly 15% of its value to settle near the $5,000 mark. To the casual observer, this seems nonsensical—why sell the ultimate safe haven during a hot war?

The answer lies in The Liquidity Squeeze. As global equity markets and digital assets plummeted, institutional traders faced massive margin calls. To cover these losses, they were forced to liquidate their most "profitable" and liquid positions—which, following the rally of late 2025, was gold. Furthermore, the oil-driven inflation spike has forced the Federal Reserve to signal even higher interest rates. Because gold pays no yield, the "opportunity cost" of holding it has skyrocketed alongside the U.S. Dollar, which has emerged as the true "Fortress Asset" due to American energy independence.

Conclusion

We are no longer pricing "risk"; we are pricing "operational capacity." The closure of the Strait of Hormuz has moved the global economy from a period of "Just-in-Time" efficiency to "Just-in-Case" survival. For investors, the takeaway from March is clear: when the arithmetic of energy supply breaks, the old rules of safe-haven investing are the first casualties.

The "Rate Paradox" has met the "war reality." Governments may need low rates to fund this conflict, but as long as Oil remains at $116, the inflation fire will keep the Fed's hands tied, and gold will remain a casualty of the very liquidity crisis it was meant to hedge.