Silver Breaks $100: What I Learned Waiting 7 Years | Deriv

In 2018, I bought physical silver convinced it should hit $100. After seven years of patience, supply deficits and demand finally delivered.

By Prakash Bhudia · Global Trading Strategist & Technical Markets Expert

26 January 2026 · 5 min read

In 2018, I bought 1 tonne of physical silver. At the time, I recall global annual production was around 24,000 tonnes. I remember doing the math and thinking: "I'm a nobody, and I just bought a tonne.” If 23,999 other people around the world decided to do the same, there would be no silver production left for the year. Something was definitely wrong with this market.

I had read all the books, watched every Mike Maloney video, done my research. I was convinced silver should be trading well above $100. Back in 2018, my line was: 'Silver will seem plentiful until it suddenly isn't.”

And then I waited. And waited. Years of disappointment followed. The price went nowhere. Some may say it was because of "price suppression.” I even questioned whether the correction would happen during my lifetime.

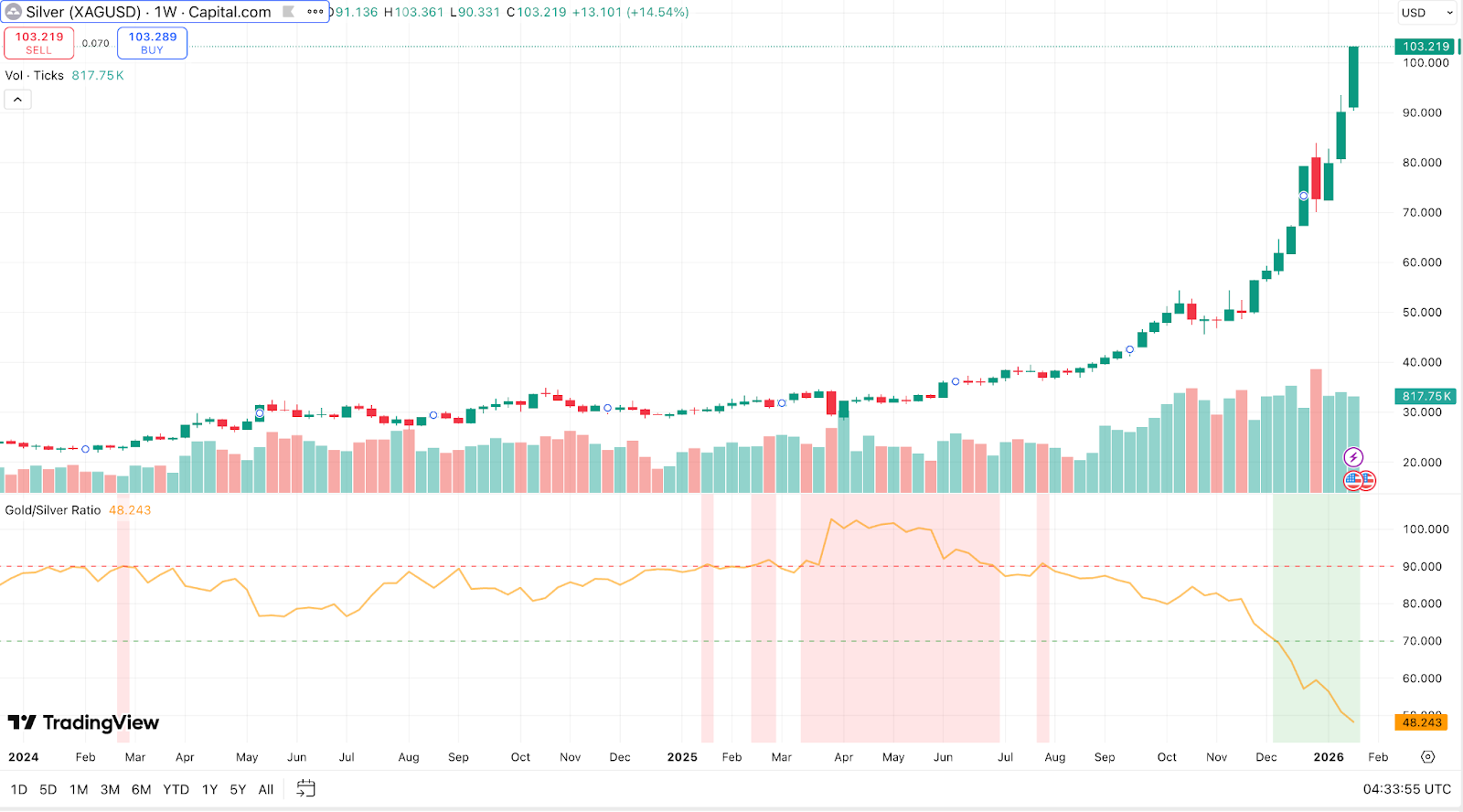

After years of no action, what I dreamt about for years finally happened this week. Silver closed above $100 for the first time in history, briefly touching $102.87 on Jan 23. The move came, but even I was taken aback by the ferocity. Here are my thoughts on what drove it.

The numbers

Silver surged 147% in 2025—the largest annual gain on record going back to 1983—and added another 40% in the first weeks of 2026. The previous all-time high was $49.51 in 2011. This move more than doubled that. Gold also rallied to $5,000/oz, but silver outpaced it significantly. The gold-to-silver ratio compressed to 50:1, the tightest since 2011. As recently as April 2025, it took over 100 ounces of silver to buy one ounce of gold.

In inflation-adjusted terms, silver would need to hit roughly $150 to match its 1980 peak. So while this is historic in nominal terms, the real value is still below that earlier spike. But the velocity of this move is what matters.

Three forces converged

Safe-haven demand

Silver benefited from the same macro drivers that lifted gold: dollar weakness, declining real rates, inflation concerns, and geopolitical risk. But silver’s lower unit price—a fraction of gold's $5,000—made it accessible to retail. This amplified participation massively.

ETF holdings surged. The Silver Institute reported a 187 million ounce increase in global ETF holdings through 2025. Anticipated U.S. tariffs on silver imports triggered massive inflows into U.S. warehouses, draining liquidity from London.

Retail demand was the differentiator. Waves of small investors buying physical coins, bars, and ETF shares drove momentum, particularly in Q4 2025. In China, silver contracts on the Shanghai Gold Exchange traded at record premiums. The country’s only pure-play silver fund stopped accepting new capital after repeated risk warnings. Western coin dealers reported the same frenzy. This resembled the 2021 #SilverSqueeze but with far greater scale because fundamentals supported it.

The Fed's pivot to rate cuts in late 2025 lowered the opportunity cost of holding non-yielding assets. With inflation above target and government debt elevated, investors sought tangible stores of value. Silver's affordability made it "poor man's gold."

Supply deficit

Unlike gold, silver derives significant value from industrial applications. It's critical in electronics, solar energy, EVs, and high-tech sectors. Industrial demand has been climbing. Supply has not kept pace.

Solar power is the largest industrial consumer—over 100 million ounces globally in 2025 despite manufacturers reducing silver content per panel. Each electric vehicle uses 1-2 ounces of silver. One strategist estimated that data centers and tech hardware in the U.S. and China alone consumed around 350 million ounces in 2025—over half of annual global mine output.

The problem is structural. Most silver is produced as a by-product of mining other metals like lead, zinc, copper, and gold. Only 25-30% of silver mines are primary producers. You cannot easily increase copper mining just to extract more silver. Mine output in 2025 was nearly flat at 813 million ounces despite soaring prices.

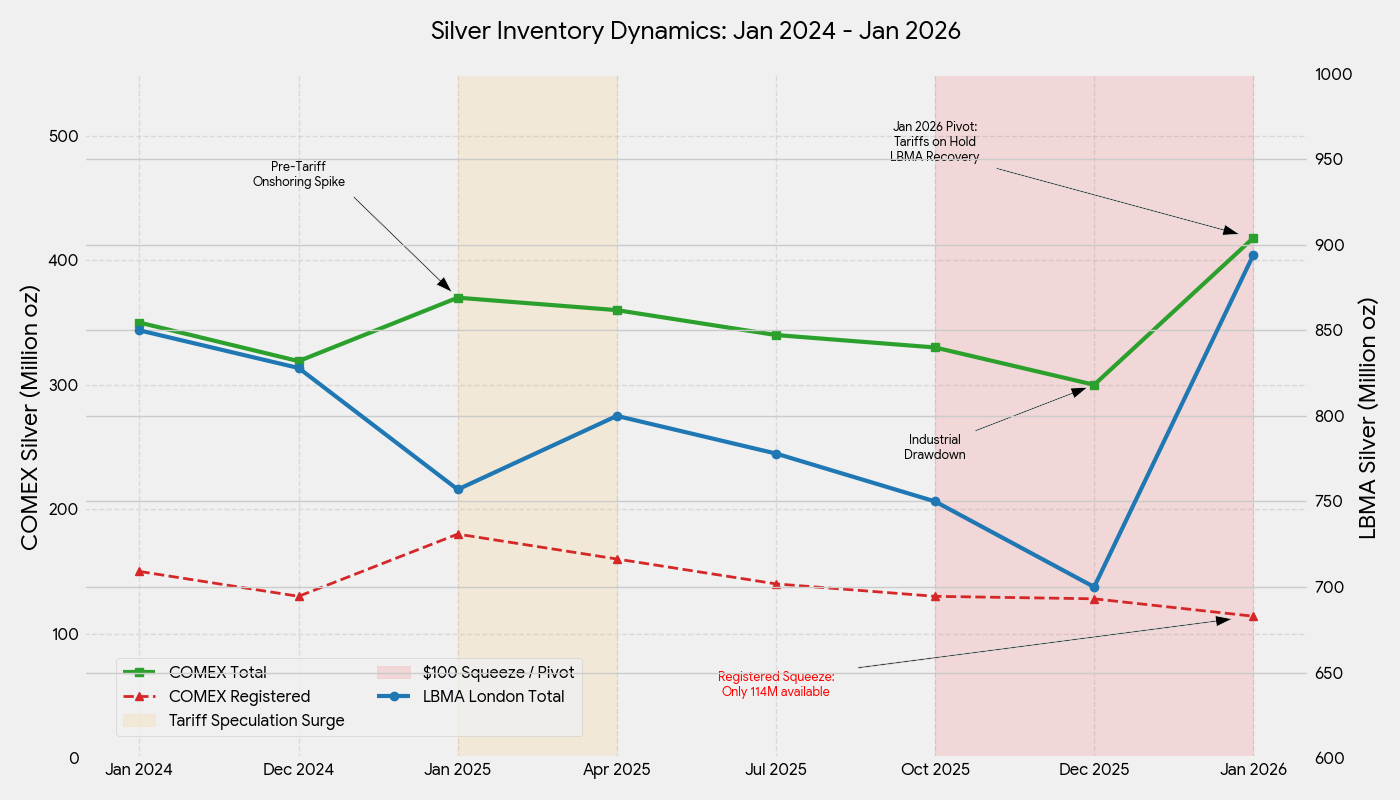

Making matters worse, much of the world's silver refining happens in China. The country controls 60-70% of global refined silver supply, importing ore and concentrates, refining domestically, and exporting finished bullion. On January 1, 2026, China implemented new export controls requiring government licenses to ship silver overseas. Only 44 large entities meeting strict production and financial thresholds can now export. This effectively gave China the ability to prioritize domestic supply right as the rally was peaking, further starving Western markets of refined metal.

For the fifth consecutive year, silver demand outstripped supply. The 2025 deficit was 95 million ounces. From 2021-2025, the world consumed roughly 820 million ounces more silver than was produced. Recycling, which accounts for about 20% of supply, ticked up modestly, but refining capacity constraints limited scrap processing.

This created severe inventory drawdowns. London's LBMA vaults held only 136 million ounces of immediately deliverable silver by end-September 2025—the lowest on record. Silver lease rates hit multi-decade highs. New York's COMEX saw the reverse initially due to tariff-driven inflows, peaking at 532 million ounces in October. But as prices climbed and tariff fears subsided, flows reversed. By mid-January 2026, COMEX stocks fell to 418 million ounces—a drop of 114 million ounces in a few months, equivalent to $11 billion withdrawn.

Even at doubled prices, physical buyers kept calling for delivery. Classic supply squeeze.

Short squeeze

Tight supply and frenzied buying put enormous pressure on short sellers. As prices surged past $50, $60, $80, and towards $100, traders betting against silver were forced to cover positions, pushing prices higher.

Exchanges intervened. In late December, COMEX hiked margin requirements, forcing traders to post more capital. Many smaller speculators trimmed positions, contributing to a sharp 9% pullback on December 29. That dip lasted one day. Silver resumed climbing as the fundamental squeeze remained intact.

Retail coordination amplified this. Online forums discussed a "silver squeeze" and theories about price suppression. Slogans like "$100 is just the beginning" circulated. Some analysts argued silver remained undervalued even at $100, with extreme views targeting $300-400. This sentiment discouraged selling and reinforced the squeeze.

Short sellers found themselves trapped. The more prices jumped, the more they had to buy back. This feedback loop turned a steady uptrend into a near-vertical spike in late 2025.

What comes next trading strategies market analysis experts

After nearly tripling in a year, the question is whether this holds.

Correction risks

Technical and fundamental indicators suggest silver is overbought. Parabolic moves often invite sharp pullbacks. The 9% drop in December when leveraged longs took profits demonstrated this risk.

Demand destruction is a concern at $100. Industrial users are seeking substitutes. Bank of America's team estimated a "fundamentally justified" price closer to $60, implying significant speculative premium. Demand from sectors like solar may have peaked as high prices force efficiency measures. Jewelry demand also drops at elevated prices.

Market sentiment turning is the bigger risk. Rhona O'Connell of StoneX said the market is in a "self-propelled frenzy" now flashing warnings. In her words, "as and when cracks start to appear they could easily become chasms—buckle up." The gold-to-silver ratio at 50:1 suggests silver may be stretched. BNP Paribas warned that "profit taking is likely sooner rather than later."

Structural supports

The structural drivers—robust industrial demand and constrained supply—do not resolve overnight. Metals Focus expects the supply deficit to persist in 2026. Inventories remain relatively scant. Primary silver miners are enjoying fat profit margins (all-in sustaining costs often below $20/oz), but new projects take years.

The macro backdrop remains bullish for precious metals. Silver is benefiting from safe-haven momentum and industrial growth themes. Unless there's a sharp global recession, this dual role continues attracting buyers. The Fed's easier stance and central bank gold purchases are tailwinds that persist.

With Washington refraining from silver import tariffs, metal hoarded in U.S. vaults is flowing back to the global market. This should improve liquidity and ease the extreme tightness. But this metal is filling gaps elsewhere, not creating a glut. The deficits of recent years depleted above-ground reserves. It will take a sustained surplus to rebuild them.

Final thoughts

I waited seven years for this move. The conviction was there, but the patience required was brutal. Now that it's happening, the reality is more complex than the books and podcasts suggested. Yes, the supply-demand imbalance was real. Yes, the market was small enough that retail participation could matter. But the actual catalyst was a convergence of forces—investor flows, industrial tightness, and a short squeeze—not just one narrative.

Silver's break above $100 is historic, but volatility will remain high. A correction would not be surprising. What matters is whether the structural floor has shifted higher. Based on persistent deficits, tight inventories, and ongoing industrial demand, that seems likely.

For now, after decades of waiting, silver is finally having its moment.