The AI Capital Vacuum: Why Bitcoin’s 4-Year Cycle May Break

Bitcoin's 4-year cycle is a narrative, not a mechanism. As AI infrastructure absorbs global capital, liquidity shifts may break crypto's historical patterns.

By Manaf Zaitoun · Editorial Strategy & Fintech Content Specialist

9 June 2026 · 5 min read

Have you come across a Bitcoin 12-16 year chart with random vertical lines on it? Congrats! You just met one of the most prominent narratives in the Bitcoin community: the cycle.

According to many Bitcoin enthusiasts, it’s meant to go through a rollercoaster of a bear market or crypto winter, a rebound, and then another all-time high every four years. Instructions are also clear: endure the bear market, hold steady, and ride a historical wave to a new all-time high. This time, an unprecedented technology, driving unprecedented capital flow, is very likely to break this cycle.

The great capital vacuum

A cycle is a narrative, not a mechanism — calendars don't manufacture billions in market capitalisation on schedule. Look closely at Bitcoin's historic runs, and they were rarely the product of mathematical inevitability or internal network events. They were driven by macro liquidity and external catalysts: the reaction to an Elon Musk tweet, shifting regulatory expectations after Donald Trump's election, the Federal Reserve flooding the economy with liquidity.

We tend to credit the asset's brilliance and ignore the macro spark that lit the move. Believe purely in the cycle, and you miss the more useful framing: Bitcoin is a sensitive sponge for excess global liquidity. However, a liquidity shortage looms on the horizon, and it’s very likely to happen around the rebound deadlines Bitcoin enthusiasts are pinning, which fall in Q4 2026.

To understand why risk assets may struggle over the next year, look away from crypto charts and toward the capital-extraction event unfolding in equities.

.webp)

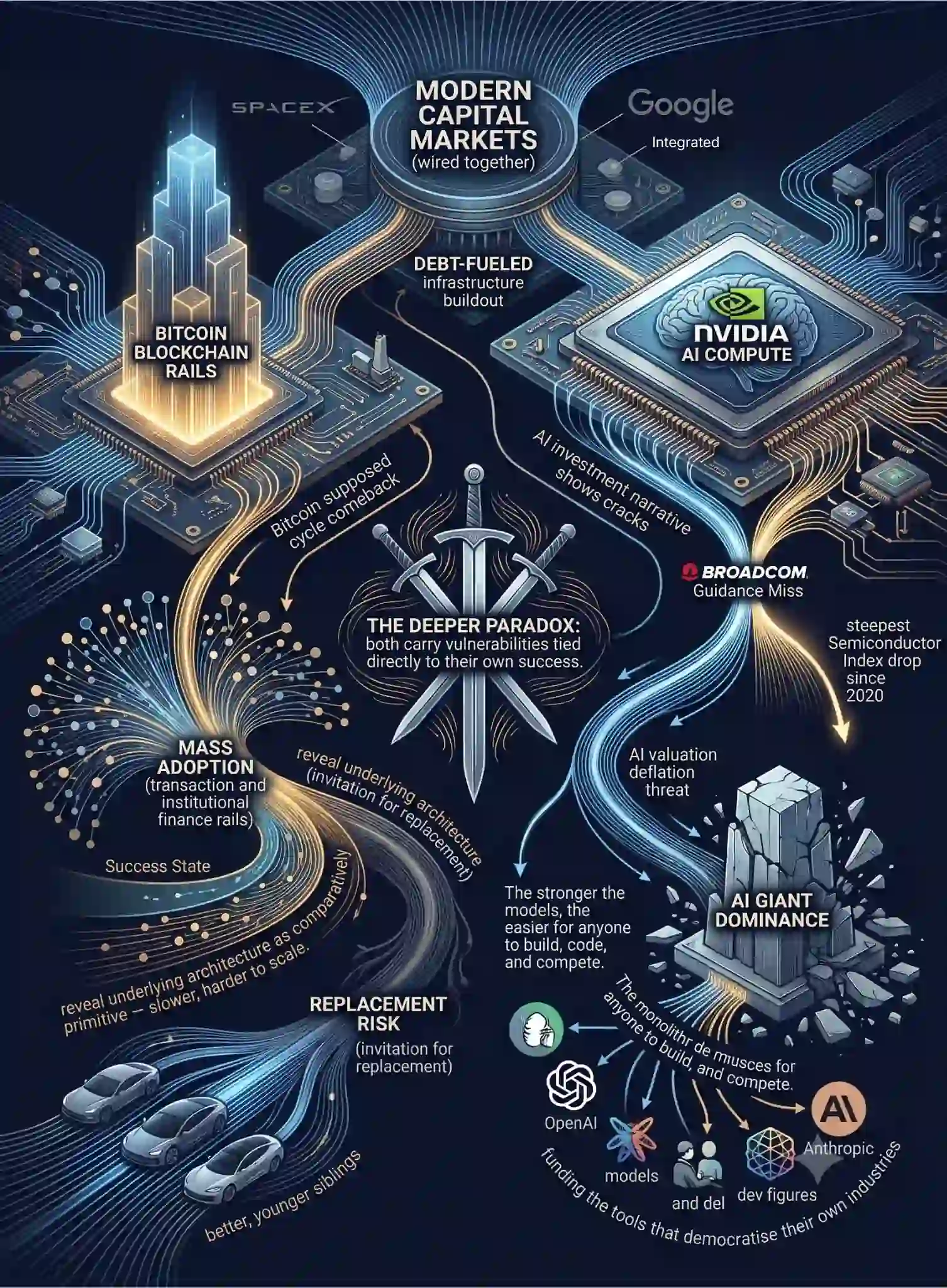

A series of enormous IPOs is about to absorb a vast amount of retail and institutional money. SpaceX is preparing the largest IPO in history, aiming to raise roughly $75 billion, with reports of attracting over $250 billion in demand already. This is only the starting gun. Behind it sit the long-awaited public debuts of AI leaders OpenAI and Anthropic, both of which have confidentially filed and are targeting listings later this year.

Beyond the IPOs, an unexpected player is competing for capital. Alphabet — already public — just priced an ~$85 billion equity raise specifically to fund its AI compute and infrastructure buildout, with Berkshire Hathaway taking a $10 billion stake at a 6% discount; another worrying signal of rising capital scarcity.

When the most promising companies in the world pull this much capital out of the system at once, liquidity dries up. Investors are unlikely to liquidate their defensive positions in healthcare, energy, and other industries with no direct connection to AI. It’s going to be the big tech and other high-risk assets to suffer the most from this capital vacuum. And while Bitcoin tends to move in harmony with tech shares, it also tends to take a larger cut of the losses.

However, this is not Bitcoin’s worst nightmare.

The hidden cost of success

Lately, AI’s investment narrative started to show some cracks. The debt-fueled infrastructure buildout hit a sharp reality check in early June, when a Broadcom guidance miss triggered a roughly $1.3 trillion single-day wipeout across chip stocks and the steepest drop in the Philadelphia Semiconductor Index since 2020.

Whether that was the first crack in a valuation bubble or a rotational shakeout is still genuinely contested — Nvidia's leadership and several big banks read it as a buying opportunity, and the sector partly rebounded. But if AI valuations do deflate toward historical multiples, the downturn would coincide neatly with Bitcoin's supposed cycle comeback.

Historically, when tech corrects hard, risk-on assets like crypto are the first thing institutions liquidate to meet margin calls. Expecting crypto to soar independently while the core tech sector suffers simply ignores how tightly modern capital markets are wired together.

The deeper paradox is that both Bitcoin and AI carry vulnerabilities tied directly to their own success. Each is a double-edged sword, where realising the core promise could undermine the current investment case.

For Bitcoin, the risk lives inside its goal of mass adoption. If decentralised blockchain technology actually becomes the rails for daily transactions and institutional finance, the market may notice that Bitcoin's underlying architecture is comparatively primitive — slower, harder to scale, and less programmable than newer ecosystems, if programmable at all. Win the adoption war outright, and it risks being replaced by better, younger siblings.

AI faces a similar, more expensive version of the same dilemma that could shatter the skyrocketing AI-powered growth — the foundational promise of the AI investment fever.

The stronger and more capable the models become, the easier it gets for anyone to build, code, and compete. The giants pouring tens of billions into infrastructure are, in effect, funding the tools that democratise their own industries.

By putting enterprise-grade cognitive capability in the hands of small startups and individual developers, they are actively eroding the advantages that made them dominant.

The industries that can most be powered by AI should expect an oil glut-style rise in supply, leading to more competitive pricing and making it harder for ends to meet, especially if predictions of a more expensive, unsubsidised AI materialise.

Bottom line, there are very few, unlikely scenarios where AI leaves enough capital for Bitcoin to thrive over the next 4 years.

Markets are governed by available liquidity and the gravity of mean reversion. Navigating the next few years will mean looking past comforting cyclical narratives to see clearly where capital is actually flowing, and more importantly for Bitcoin hodlers, whether this ultimate battle over capital would leave any liquidity surplus to fuel Bitcoin’s next rally, or hold its declining support levels to start with.