The SpaceX IPO is not just about rockets

SpaceX's record-breaking IPO values the company at $1.77 trillion. Discover why buying shares of SPCX is actually a massive bet on the infrastructure powering artificial intelligence.

By Prakash Bhudia · Global Trading Strategist & Technical Markets Expert

12 June 2026 · 7 min read

SpaceX is expected to price its initial public offering tonight and begin trading tomorrow, Friday 12 June, on the Nasdaq under the ticker SPCX. The numbers have no precedent. The company is being offered at roughly $135 a share, valuing it at about $1.77 trillion and raising on the order of $75 billion — the largest IPO ever, comfortably more than double the record Saudi Aramco set in 2019. Reported demand has run past $250 billion, several times the stock on offer, and an unusually large slice of the deal — close to a third — is said to be earmarked for retail investors, against the usual five to ten percent.

So this one will land in a lot of ordinary portfolios. Before it does, it is worth being clear about what is actually being sold. Despite the name, this is not really a bet on rockets.

What you're actually buying

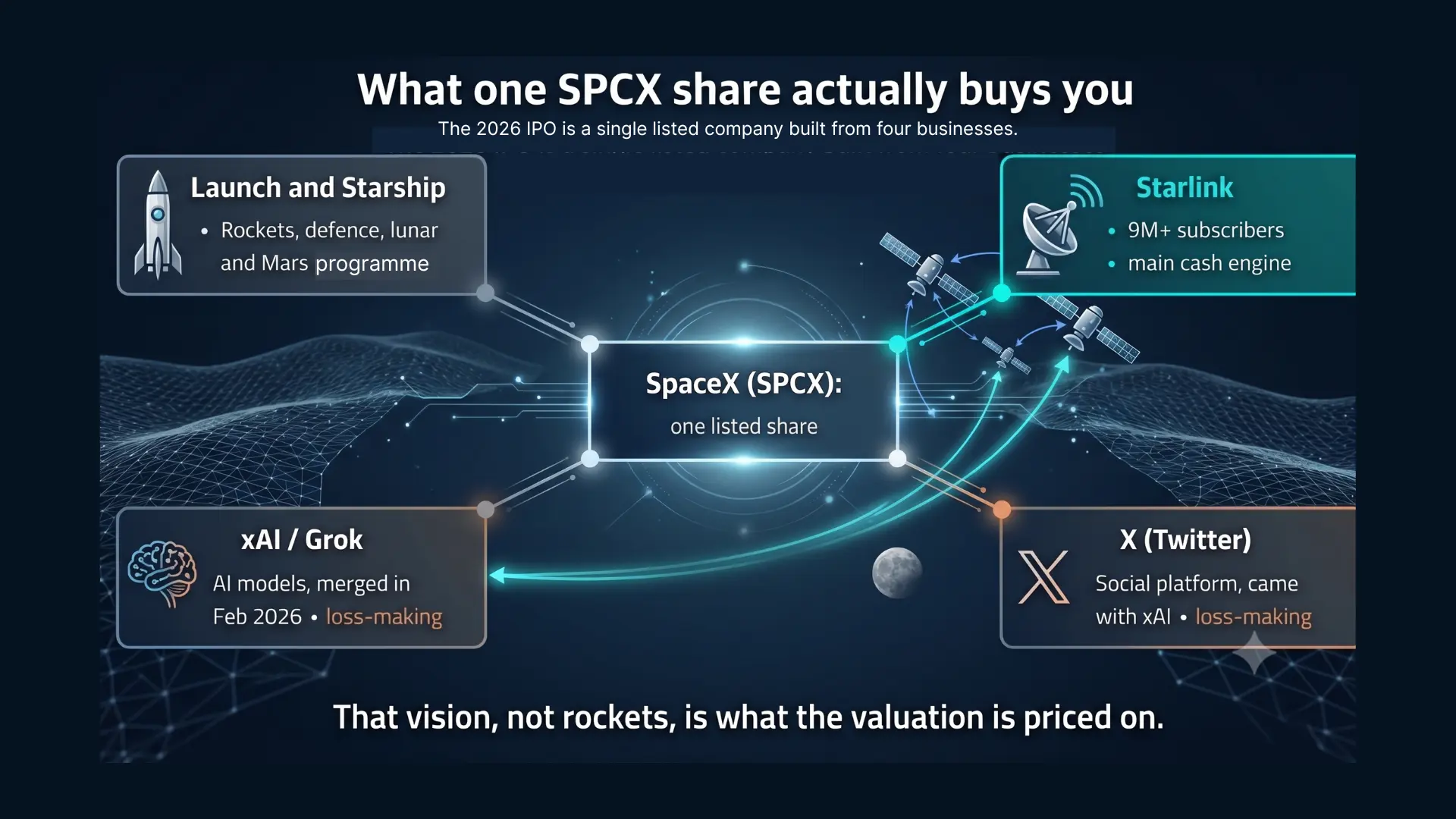

In February, SpaceX absorbed Elon Musk’s AI company, xAI — which had itself already swallowed X, the platform formerly known as Twitter — in an all-stock deal that valued the combined group at around $1.25 trillion. That corporate reshuffle is the whole story. When you buy a share of SPCX tomorrow, you are buying four businesses bolted together: the launch and Starship operation; Starlink, the satellite-internet network with more than nine million subscribers that generates most of the group’s cash; xAI and its Grok models; and X itself. Two of those four — xAI and X — lose money today.

The logic that ties them together is not rockets. It is artificial-intelligence infrastructure. The stated plan is to pair Starlink’s satellite mesh with xAI’s models to push AI computing into orbit, where solar power is constant and the cold of space handles the cooling. Whether or not that vision is ever fully built, it is what the valuation is priced on. SpaceX is being sold to the market as an AI-infrastructure company that happens to own the world’s best rockets — not the other way around.

Why scarcity is back in public markets

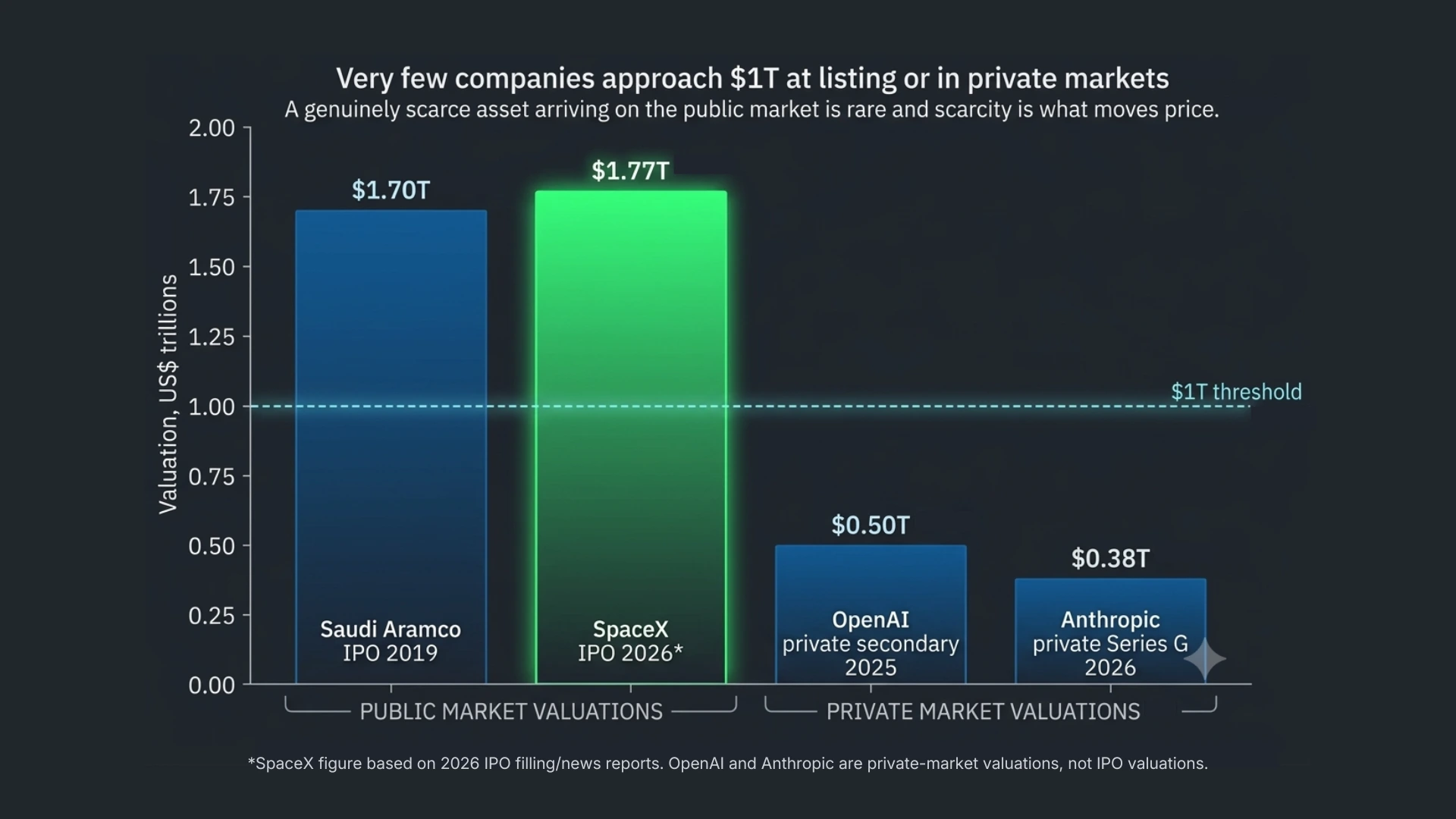

To understand the appetite, look at the company this listing keeps. For most of the last decade the most valuable technology was built and held privately. OpenAI, Anthropic and SpaceX itself compounded in value while staying off public markets, so everyday investors had no way in. A genuinely scarce asset arriving on the public market is rare — and scarcity is what moves price. This is the latest and largest in a wave of mega-listings that has been building for years.

Compute is the new oil

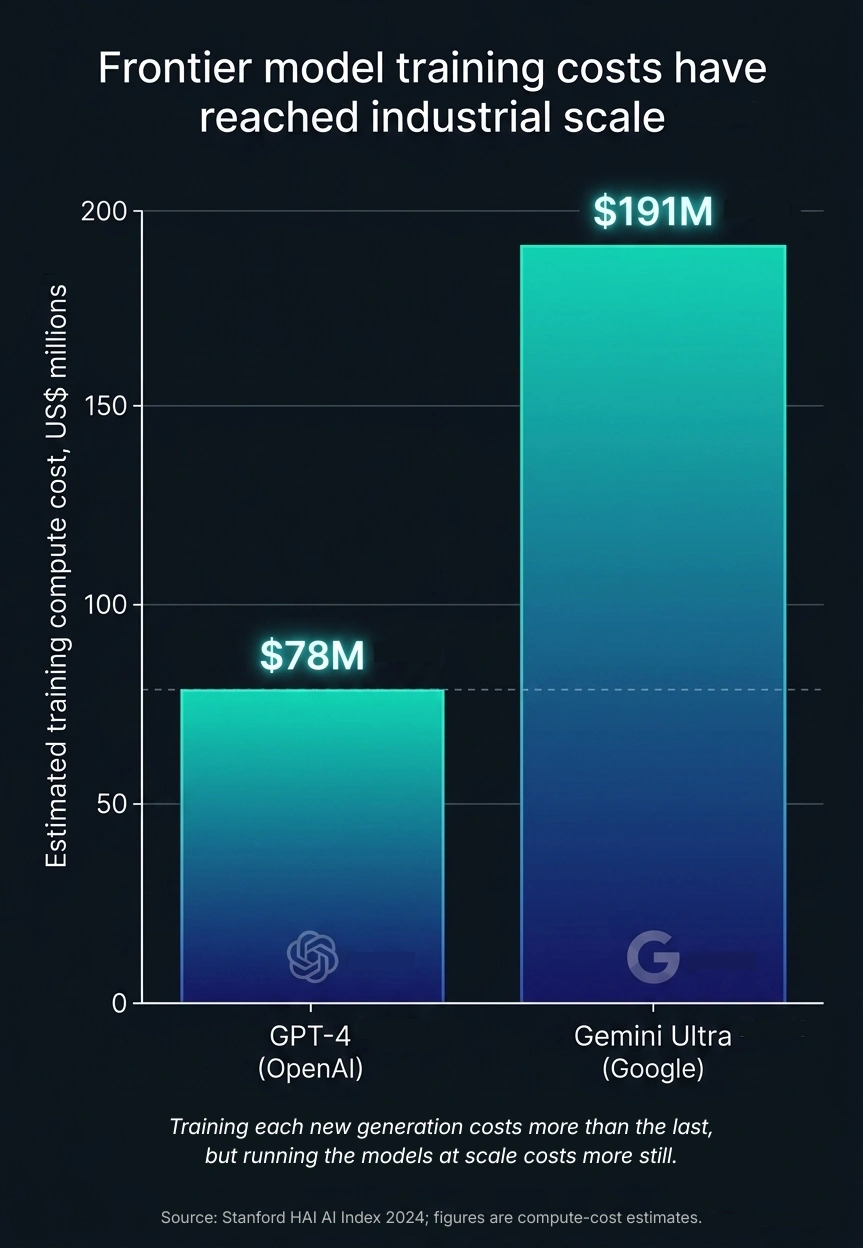

Every AI product sits on a stack. At the top are the apps people touch; below them the models — Claude, GPT, Gemini, Grok; and underneath those, the part almost nobody sees: the compute, the data centres, the cooling and the power. Training a model is expensive, and the cost climbs with every generation: Stanford’s HAI institute put the compute bill for training GPT-4 at roughly $78 million and Google’s Gemini Ultra at around $191 million. But a training run is a one-off. The larger and more durable cost is running those models for hundreds of millions of people every day — and the data centres, power and cooling that make both possible. Whoever controls that infrastructure controls the economics of the entire industry.

Power is the real ceiling

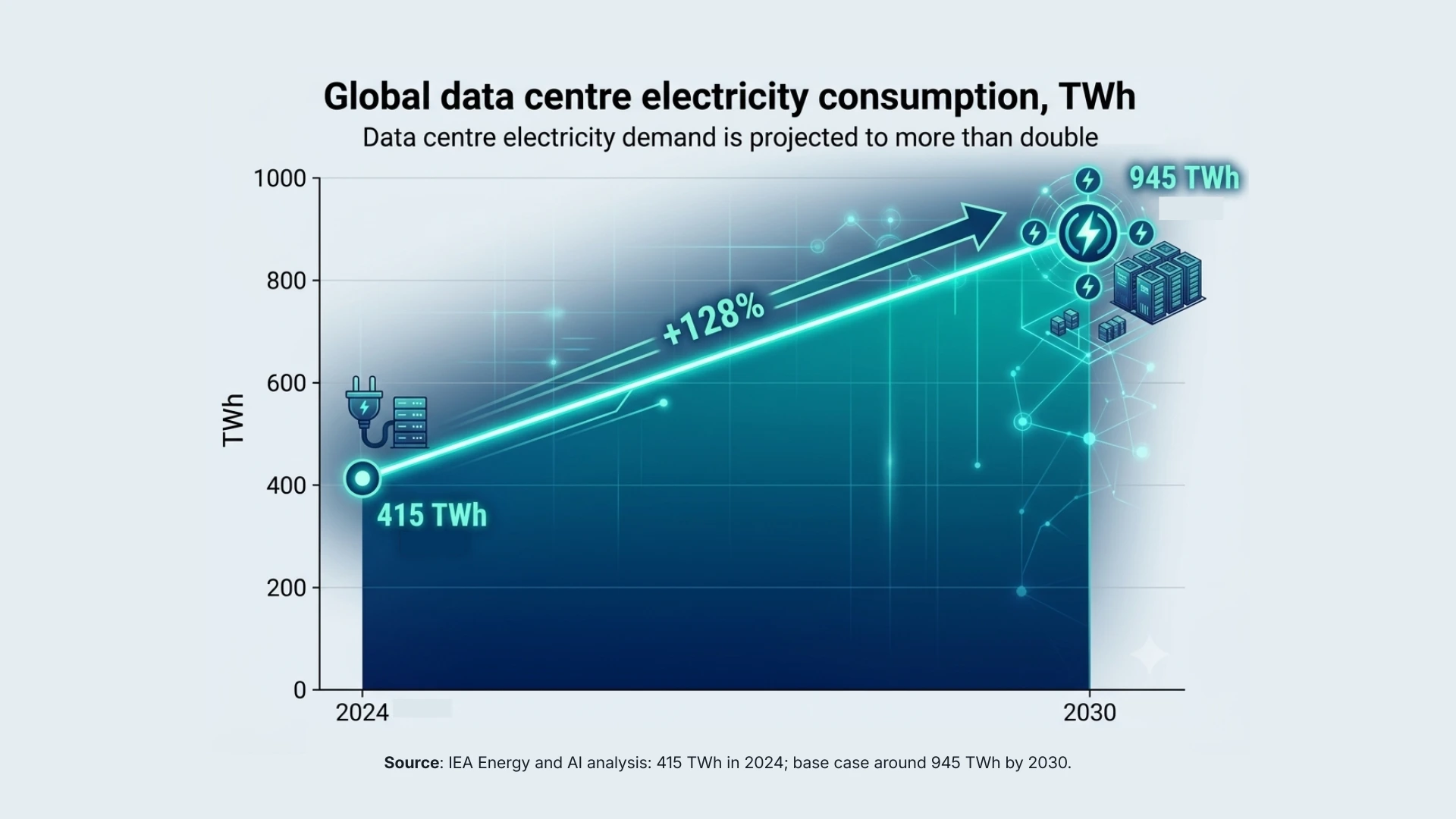

The binding constraint on AI is not chips — it is electricity. The International Energy Agency estimates data centres consumed about 415 terawatt-hours in 2024 and could reach roughly 945 terawatt-hours by 2030, with Goldman Sachs projecting data-centre power demand rising on the order of 165 percent over the decade. That is the bottleneck that makes “free” orbital solar power more than a slogan in the pitch: if power is the limit on the ground, moving compute to where the sun never sets is a genuine strategic angle, however far off.

The unglamorous part: heat

The other physical limit is heat. Packing chips densely enough to train large models means the older approach of blowing cold air around a room no longer keeps up; operators are shifting to liquid running directly across the hardware. It is the least glamorous corner of the AI story, and it is exactly the kind of physical, infrastructure-level problem SpaceX is positioning around — power and cooling, not prompts and chatbots.

A reality check on the price

All of which explains the ambition — but not whether the price is sane. At about $1.77 trillion on perhaps $18 to $19 billion of revenue, SPCX is being valued at a multiple of earnings several times richer than Meta, Alphabet or Nvidia, and well above even Tesla at its most stretched. The valuation has roughly quintupled in twelve months, from around $350 billion in May 2025 to $1.25 trillion at the February merger to about $1.77 trillion now. You are also paying for two loss-making businesses inside the package, under a governance structure where Musk controls roughly 85 percent of the votes and now runs two trillion-dollar companies at once. Analysts have called it the most divisive IPO in a decade.

None of that means the stock won’t rise. It means the margin for error is thin: the price already assumes the orbital-AI story works.

The $1 trillion to $5 trillion question

Joining the trillion-dollar club is close to confirmed at this price. Holding there is harder. Reaching $5 trillion — a level only Nvidia has touched in recent memory — would take category dominance and profits large enough to justify it, sustained over years rather than proven on one strong opening day. It is the difference between a milestone and a guarantee.

How to think about it

Rather than forecasting, it helps to hold a few scenarios loosely. In a weaker case, the infrastructure thesis takes longer than the price assumes, the loss-makers stay losses, and an over-subscribed open fades — first-day pops in heavily hyped listings often do. In a base case, Starlink’s cash and launch dominance support the valuation while the orbital-compute story develops slowly in the background. In a stronger case, SpaceX becomes the toll road for AI’s physical layer — power, launch and satellite mesh — and today’s price looks cheap in hindsight. Reasonable people weight these very differently, which is precisely why the stock is divisive.

For retail investors, a few mechanics matter as much as the thesis. Allocations in hot IPOs are routinely scaled back, so you may receive far fewer shares than you ask for. The opening trade can sit well above the offer price. Early volatility tends to be high, and day-one “flipping” pressure can cut both ways.

The bottom line

The headline says rockets. The valuation says AI infrastructure. The honest description is that SPCX is a high-conviction, high-price bet that one company will own a meaningful share of the physical layer the AI era runs on — compute, power, cooling and the satellite network to stitch it together — with a profitable rocket-and-internet business underneath to fund the wait. That may prove visionary or merely expensive. Tomorrow’s open will tell you what the market feels, not whether the thesis is right.

This article is market commentary intended for educational purposes only. It is not investment advice, nor a recommendation or solicitation to buy or sell any security.

All figures are based on pre-listing reporting and market estimates and may change when final prospectus pricing is confirmed. Trading and investing carry risk, including the possible loss of capital.